Futures Market: Overnight, LME copper opened at $9,469.5/mt, initially touching a high of $9,480/mt. It then fluctuated downward throughout the session, hitting a low of $9,405/mt, before rebounding slightly at the close to finish at $9,446.5/mt, up 0.44%. Trading volume reached 16,000 lots, and open interest stood at 284,000 lots. Overnight, the most-traded SHFE copper 2506 contract opened at 77,950 yuan/mt, maintaining a narrow range and touching a low of 77,660 yuan/mt. It rebounded at the close to finish at 77,740 yuan/mt, up 0.19%. Trading volume reached 29,000 lots, and open interest stood at 164,000 lots.

【SMM Copper Morning Meeting Summary】News: (1) The International Copper Study Group (ICSG) held a meeting in Lisbon, Portugal, on April 25, 2025. In 2025, world mine production is expected to grow by 2.3% to 23.5 million mt, primarily driven by additional output from expansions at Kamoa (DRC) and Oyu Tolgoi (Mongolia), as well as the start-up of the new Malmyz mine (Russia). These gains will be partially offset by expected declines in Australia, Indonesia, and Kazakhstan.

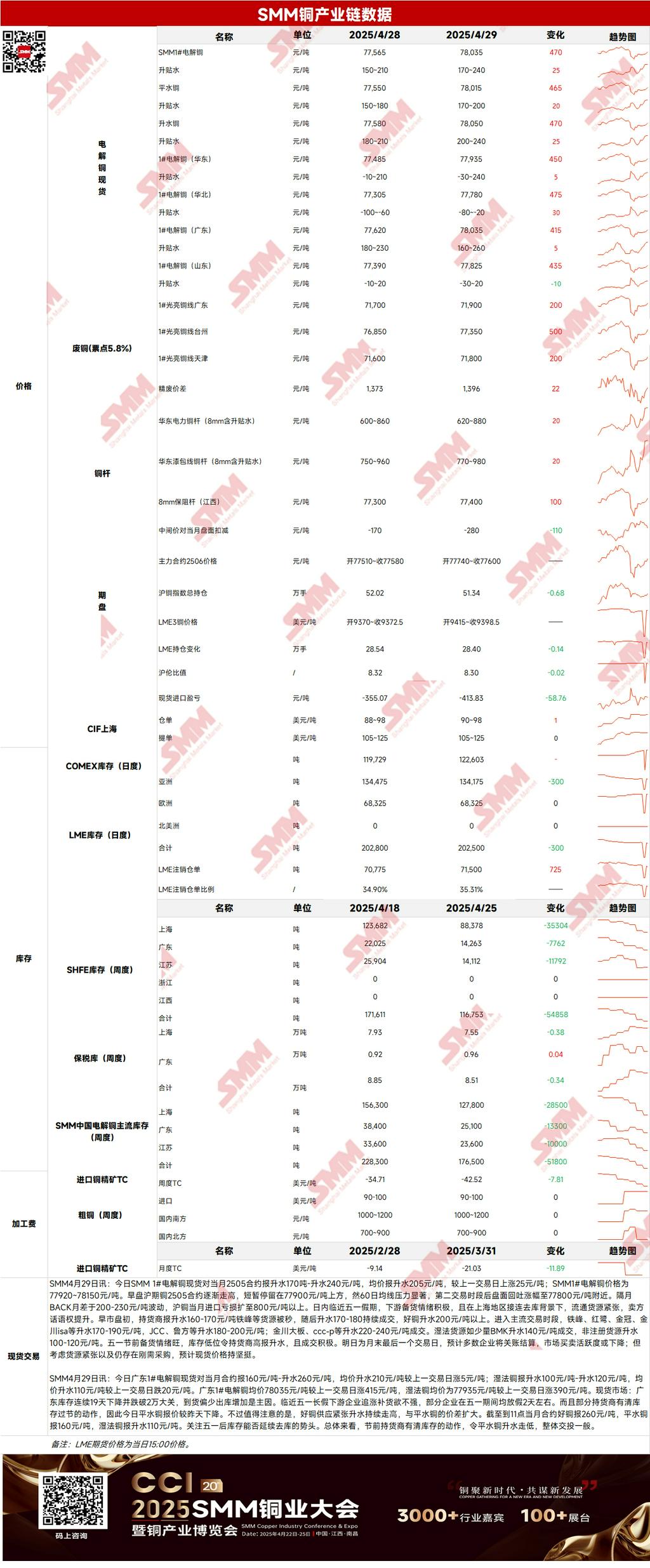

Spot Market: (1) Shanghai: On April 29, SMM #1 copper cathode spot prices against the front-month 2505 contract were reported at a premium of 170-240 yuan/mt, with an average premium of 205 yuan/mt, up 25 yuan/mt from the previous trading day. The SMM #1 copper cathode price was 77,920-78,150 yuan/mt. In the morning session, the SHFE copper 2505 contract gradually rose, briefly staying above 77,900 yuan/mt, but faced significant pressure from the 60-day moving average. After the second trading session, the futures market gave back gains to around 77,800 yuan/mt. The backwardation spread between futures contracts fluctuated between 200-230 yuan/mt, and the import loss for SHFE copper front-month contracts widened to over 800 yuan/mt. Today is the last trading day of the month, and most enterprises are expected to close their books for settlement, potentially reducing market trading activity. However, given tight supply and ongoing just-in-time procurement, spot prices are expected to remain firm.

(2) Guangdong: On April 29, Guangdong #1 copper cathode spot prices against the front-month contract were reported at a premium of 160-260 yuan/mt, with an average premium of 210 yuan/mt, up 5 yuan/mt from the previous trading day. SX-EW copper was reported at a premium of 100-120 yuan/mt, with an average premium of 110 yuan/mt, down 20 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 78,035 yuan/mt, up 415 yuan/mt from the previous trading day, while the average price of SX-EW copper was 77,935 yuan/mt, up 390 yuan/mt from the previous trading day. Overall, suppliers reduced inventory ahead of the holiday, leading to lower premiums for standard-quality copper and generally moderate trading activity.

(3) Imported Copper: On April 29, warrant prices were $90-98/mt, with QP May, up $1/mt on average from the previous trading day. B/L prices were $105-125/mt, with QP May, unchanged on average from the previous trading day. EQ copper (CIF B/L) was $65-75/mt, with QP May, unchanged on average from the previous trading day, with quotes referencing port arrivals in early May. Overall, both buyers and sellers were active ahead of the holiday. It should be noted that the LME's near-month backwardation structure has widened, and significant domestic destocking will attract continued cancellations of LME Asian warrants.

(4) Secondary Copper: On April 29, the price of secondary copper raw materials rose by 200 yuan/mt MoM. Guangdong bare bright copper prices were 71,800-72,000 yuan/mt, up 200 yuan/mt MoM from the previous trading day. The price difference between copper cathode and copper scrap was 1,396 yuan/mt, up 23 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,030 yuan/mt. According to SMM survey data, imports of secondary copper raw materials in March showed that US supplies had declined to 22,000 mt, with Japan becoming the primary source of China's secondary copper raw material purchases. Given the current tense trade relations between China and the US, port arrivals from the US are expected to decrease further in April and May.

(5) Inventory: On April 29, LME copper cathode inventory decreased by 300 mt to 202,500 mt. On the same day, SHFE warrant inventory decreased by 2,842 mt to 3,404 mt.

Price: On the macro front, US job openings in March fell to their lowest level since September last year, US consumer confidence in April plunged to a near five-year low, and the US goods trade deficit in March widened to a record $162 billion. Economists have stated that the widening trade deficit could drag Q1 GDP growth down by 1.9 percentage points, with market concerns emerging. On the fundamental front, as the Labour Day holiday approaches, downstream stockpiling has been active, with continuous destocking in the Shanghai region, tightening spot market supply and strengthening sellers' bargaining power, leading to higher spot premiums for copper cathode. Today is the last trading day of the month, and most enterprises are expected to close their books for settlement, potentially reducing market activity. However, due to tight supply and ongoing just-in-time procurement, spot prices are expected to remain firm. In terms of price, with robust downstream stockpiling ahead of the holiday and concerns about tight supply, copper prices are expected to have upside room today.

【The information provided is for reference only. This article does not constitute direct investment research or decision-making advice. Clients should make cautious decisions and not rely solely on this information, as any decisions made are independent of SMM.】